(310) 550-6304

The Next Five Years

by Kenneth J. Gerbino

July 2009

There are always major and minor causes to all effects. When one is dealing with the stock market and the economy the major causes that run the show are:

- Money Supply

- Interest Rates

- Government Intervention (taxes, regulations, permits, trade barriers, etc.)

- Government Spending (high or low percent of GDP, deficit policies etc.)

The above, in turn, influence the following:

- GDP

- Stock Prices

- Employment Rates

- Inflation Rates

Unfortunately, the first four major causes in all countries are influenced by politics and this always includes insanities, stupidities and underhanded policies of the collective political power structure. Whether a democracy or dictatorship the above holds true.

Therefore to get any kind of predictive capability of the economy, stock market and precious metals one has to understand how the first four causes effect different markets. In the U.S. and most other countries the abuses of these causes have been around for decades and are now at an acute stage, therefore the effects are going to be severe.

But the effects need to be analyzed for the short, medium and long term. And this is where the difficulty really lies.

I will stick to the medium term in this article. Here are my predictions based on Austrian School economic principles. For the uninitiated the major Austrian principles are as follows:

- Two plus two equals four

- Money should not be debased

- More money equals currency depreciation and more inflation

- The free market with billions of people voting with their personal interests of needs and wants should not be tampered with and is the best and most efficient allocator of economic resources.

- Interest rates should never be left to the government or central banks to manage.

- Trade should be wide open between countries so consumers get the best price for their pay check.

- Price levels should be based on subjective values – meaning if you are thirsty in the desert you will pay more for water and the market will get water to that location.

- There are many more but this is the simple list

- Government intervention in any market is inefficient and counterproductive.

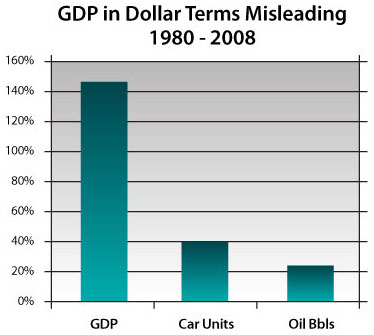

Unfortunately, our world is very far away from these sound economic principles so one has to have a game plan to survive with ones savings and investments. Below is a graph which shows how misleading GDP numbers are. Here you would think the U.S. economy has expanded over 140% since 1980. But in terms of real economic activity measured by real stuff one can see that it has been a mirage. Oil barrels consumed is a great indicator of economic activity since oil is used as a substance in over 100,000 products and energy consumption should parallel economic output. Here we see that oil consumed in barrels shows a 22% increase in 28 years. That means the U.S. economy probably has grown less 1% a year. GDP is distorted by paper money. Units not prices should be the guts of GDP.

Inflation – Deflation

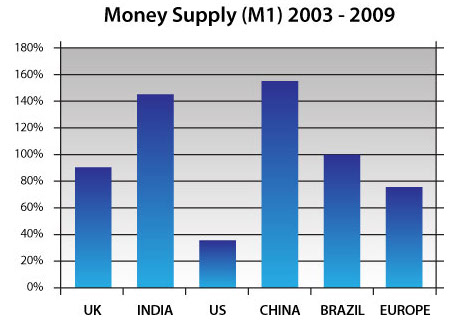

Right now the big debate is about inflation or deflation. This is always decided by money supply increases or decreases. Since the global money supply increases are excessive I really can’t see where the deflationistas have a prayer. Yes, prices have come down the last 18 months but where were prices 3-5 years ago or 10 years ago? Much lower. Expect massive inflation rates in the coming years once the money starts bubbling through the economy. Note in the graph below that the U.S. M1 money supply looks very low and this is because money in this category is actually swept out of cash and demand deposit accounts each night electronically and this understates M1. This graph also tells us that there is going to be plenty of inflation in China and India and these gold and silver loving populations are certainly going to be moving into the precious metals in a big way.

Commodities

This is very simple. Population increases, and in turn the big populations of China and India progressing dramatically toward a massive middle class demand situation will have a strong influence on commodities and raw materials for the next 30-40 years. The credit crisis has delayed many capital investments in raw material projects and this will curtail supply in the medium term. Also, money supply increases will put upward pressure on commodity prices.

Monetary Policy

This is a major influence on all investments. In the U.S. it has been reckless for almost two decades and this resulted in massive speculation and over leverage in the real estate commodity, derivatives and stock markets. This affected the entire world as international markets blended together in the last two decades via technology. The authorities were then faced with catastrophic repercussions as major financial institutions were at risk and the path of least resistance was to flood the world with money and go into a lot of debt at the same time.

A World of Debt

The debt levels in some countries are now too large to pay back. The solution will be to inflate them away.

In 10 years the $10 trillion U.S. debt won’t look so bad if hamburgers cost a few hundred thousand dollars (I am joking, but you get the picture).

Long term bonds will be a very bad place to have money when the inflation that is coming forces interest rates much higher and the value of these bonds much lower.

Psycho Markets

Leverage, greed, fear and confusion are now the order of the day. Stock markets will be prone to panics and the volatility will be extreme for many years. The gold market will benefit from this but will also be very volatile. There are now tens of millions of day traders in the world. Office workers at their desks and housewives in Indonesia are trading stocks. Professionals are married to black box analytics or technical patterns (which by the way will soon become less useful, except for the more broad based patterns). Day trading is now a global phenomenon. With instant communication and 99% of global investment professionals being clueless on Austrian School economics, you can expect a lot of confusion in world stock markets.

Your Solution

- Do not use leverage

- Divide your stock portfolio into Core positions and Trading positions. If you like XYZ then buy 1000 shares for an investment and trade 1000 shares. The days of buying and holding are over if you want to help improve your return. XYZ may stay in a trading range for 10 years. You may as well try and buy it when it is being sold off and sell it when it moves up. As long as you have done your homework and feel the company should trend higher, then a core position is worth it.

- Own some gold and silver and have it nearby in physical form.

- Own the gold and silver mining stocks. Stay with mostly medium to large producers and companies that are within a year of meaningful production. Small mining companies with small production or deposits should be avoided. They odds of being bought out are nil and they will never have an institutional following.

- Oil companies will do well as global oil supplies peak and oil demand explodes in the next decade.

- Own commodity producers and distributors

- Own Swiss Francs.

- Own consumer goods and consumer communication companies in China.

The Next Five Years

- Inflation is coming back

- The U.S. stock market will probably stay in a trading range of between 6,000 and 12,000 on the Dow for a decade or more. A bull market year will be up 10-15%, a bear market year will be down 10-15%. This will be similar to the 1966 -1982 time period when the Dow stayed between 550 and 1,000 for 16 years.

- Commodities will go much higher

- In 2-3 years inflation could be very severe and interest rates will go much higher. This will bring on another downward move in stocks.

- After interest rates and inflation peaks in 3-5 years it will be a great time to buy quality U.S. stocks again.

- Real estate will be a good buy in a few years

- China will buy gold mining companies and they will be followed by India. Why should these Central banks pay retail for gold when the can buy wholesale by having their sovereign wealth funds own gold mines and simply take the gold. This will take a lot of gold off the market and be very bullish for gold.

- Disregard all the talk about the U.S. dollar being replaced any time soon. Russia pushing for this is a joke. California’s GDP is 40% higher than Russia! Texas is 10% bigger. The U.S. dollar is going down and so will most other currencies (but not as much as the dollar since the U.S. appears to be the current major monetary sinner.

- Don’t worry about the end of the world or a great depression. Entrepreneurs, capitalism, free market players, producers and the movers and shakers of the world will find a way to make a product (and a buck) by producing and getting people something of value despite the politicians, inflations, recessions, panics and upheavals of the economy and markets. The old expression “The dogs bark but the caravan goes on”, is apt here.

I have to laugh when people write about the breakdown of western civilization where there are no goods on the shelves etc. and there is chaos everywhere. Did you ever see that CNN special a few years ago when they were following the smuggling routes between Afghanistan and Pakistan. You saw these guys in turbans and flip flops and donkeys going over these high mountain cliffs on narrow paths risking their lives. On top of one of the donkeys was a case of Coca Cola probably bound for a small village somewhere. If they can handle getting Coke where people want it in the one of the most backward places on earth, I am sure the boys at Coke will also be able to figure it out here in the good ol’ USA., if things got out of hand. Ditto for almost all other goods. Good luck.

Kenneth J. Gerbino

Kenneth J. Gerbino

& Company

Investment Management

9595 Wilshire Boulevard

Suite 303

Beverly Hills, CA 90212

Phone: (310) 550-6304

Fax: (310) 550-0814

Kenneth J. Gerbino & Company

Investment Management

9595 Wilshire Boulevard, Suite 303

Beverly Hills, California 90212

(310) 550-6304

Copyright 2004-2018 Kenneth J. Gerbino & Company. All Rights Reserved. KENNETH J. GERBINO & COMPANY and its logo are trademarks and service marks owned by Kenneth J. Gerbino & Company. Site design and maintenance by www.DesignStrategies.com.